Introduction

Hibah Amanah

Hibah is the gifting of an asset (ain) or benefit. Technically, it is a contract of gifting property from one person to another during their lifetime without expecting any compensation (iwad), performed voluntarily.one voluntarily.

Shariah Ruling of Hibah

There is evidence in Al-Quran, Hadith, and Ijma concerning the encouragement of giving gifts to help and strengthen relationship.

Allah SWT says:

“And give the women (upon marriage) their (bridal) gifts graciously. But if they give up willingly to you anything of it, then take it in satisfaction and ease.

(Surah an-Nisa’, 4)

Source: Saheeh International Translation

Narrated by Abi Hurairah, the Prophet (may peace be upon him) said:

"Give presents to one another for this would increase your mutual love."

(Hadith narrated by Abi Hurairah, Ahmad bin Al-Husayn bin 'Ali bin Musa Abu Bakr al-Bayhaqi, Sunan al Bayhaqi al-Kubra, volume 6, Hadith no 11726)

Conditional Hibah

There are two types of conditional hibah:

Hibah Umra

Granting ownership of property for a period (tawqit) subject to the life of the Donee or the Donor. The property will be returned to the Donor or his heirs in the event of death.

![<p data-pm-slice="1 1 []"><span style="color:#193CEB;">Hibah Umra</span></p>](https://asnb.gix.my/uploads/kelebihan_5afec21525.svg)

Hibah Ruqba

The giving after the death of one of the parties, either the Donor or Donee, as a condition of ownership to one of the living parties. The property will belong to the Donee upon the death of the Donor. However, if the Donee dies before the Donor, the property will return to the Donor.

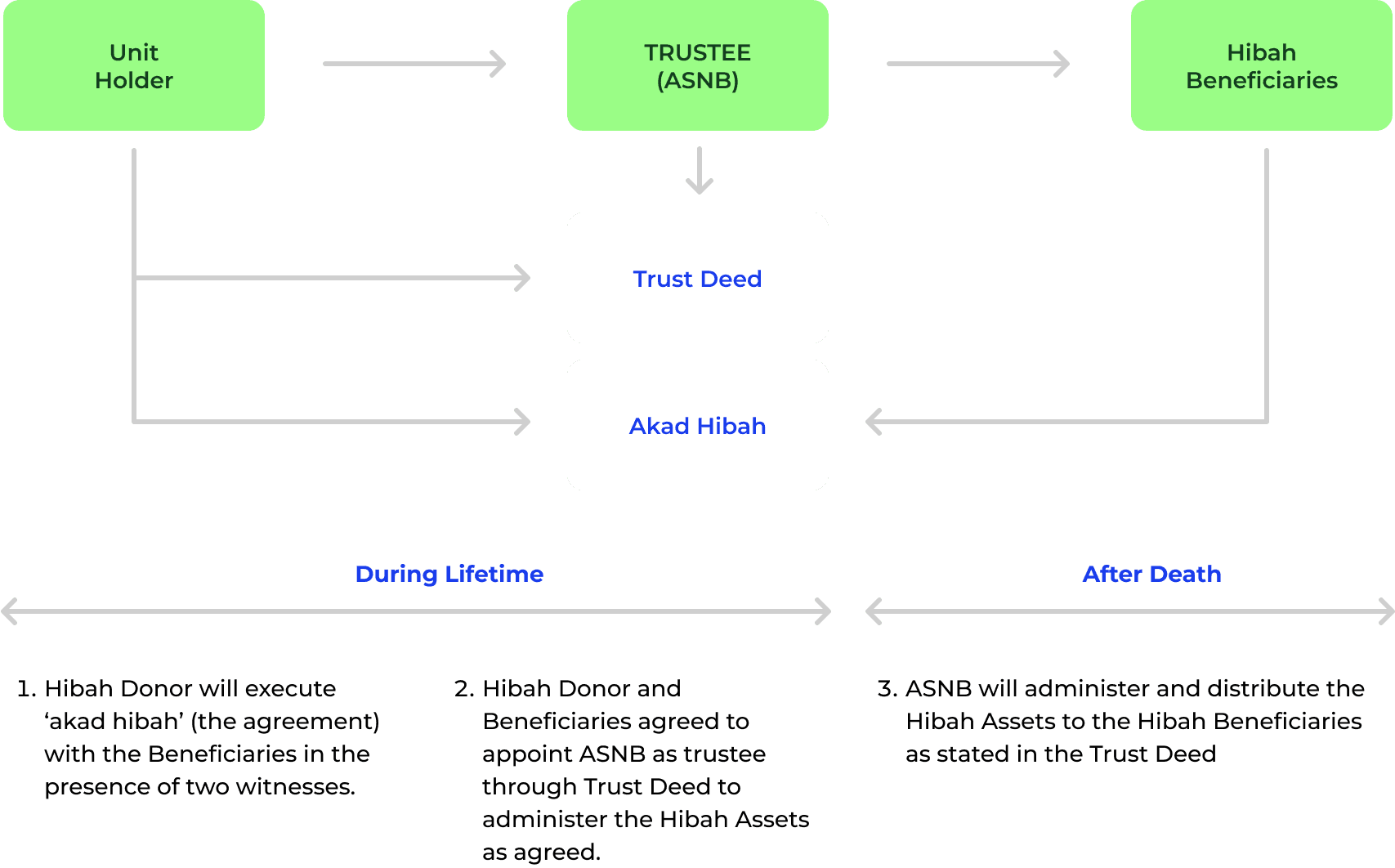

ASNB's Hibah Amanah service adopts the Hibah Ruqba approach that is refined according to the Shariah principles and meets the needs of ASNB’s unitholders, in the event the Donee dies before the Donor.

Concept

Eligibility Requirement

![<p data-pm-slice="1 1 []">Muslim Malaysian Unit Holders age 18 years old and above.</p>](https://asnb.gix.my/uploads/tick_db6cc73723.svg)

Open to all eligible ASNB funds.

Comparison of Claim Process

Advantages of Hibah Amanah

Unit Holders determine the beneficiaries and its distribution.

![<p data-pm-slice="1 1 []"><span style="color:#193CEB;">Unit Holders determine the beneficiaries and its distribution.</span></p>](https://asnb.gix.my/uploads/asnb_online_platforms_Lengkapkan_dab6b3d5d2.png)

Beneficiaries are the absolute receivers.

![<p data-pm-slice="1 1 []"><span style="color:#193CEB;">Beneficiaries are the absolute receivers.</span></p>](https://asnb.gix.my/uploads/hukum_pelaburan_Muzakarah_Jawatankuasa_Fatwa_Majlis_Kebangsaan_bd54a708e4.png)

Yuran perkhidmatan yang kompetitif.

Competitive service fees.

Letter of Administration or Grant of Probate is not required.

![<p data-pm-slice="1 1 []"><span style="color:#193CEB;">Letter of Administration or Grant of Probate is not required.</span></p>](https://asnb.gix.my/uploads/Labur_dengan_disiplin_5715ad8c67.png)

Unit Holder still retains control and enjoy the investment benefits while alive.

![<p data-pm-slice="1 1 []"><span style="color:#193CEB;">Unit Holder still retains control and enjoy the investment benefits while alive.</span></p>](https://asnb.gix.my/uploads/registration_Auto_Labur_f2e839e4cf.png)

Without Hibah Amanah

Terms & Conditions

Beneficiaries (Hibah Donees)

Individuals

Limited up to 10 Hibah Donees.

A legal guardian must be appointed if the Hibah Donee is below 18 years old.

![<p data-pm-slice="1 1 []"><span style="color:#193CEB;">Beneficiaries (Hibah Donees)</span></p>](https://asnb.gix.my/uploads/Penerima_4843574e02.png)

Donor

Muslim Malaysian Unit Holders age 18 years old and above.

Have a minimum investment balance of 1,000 units (excluding units under financing / collateral / EPF Members Investment Scheme).

- 1,000 units must be maintained in the respective fund/s during the period of the Hibah Amanah.

General Terms & Conditions

100% of absolute and wholly-owned units must be assigned to all listed Hibah Donees.

Units invested through financing / collateral are subjected to the agreement between the unit holder and the financial institution.

Revocation of Hibah can only be done if it involves Hibah grant for biological child and grandchild or for other Donee(s) by mutual consent between Hibah Donor and Hibah Donee(s).

ASNB has the right to withdraw the Hibah Amanah agreement if there is any form of violation on the terms & conditions by the Hibah Donor and if the Hibah Donor is no longer eligible to be a ASNB Unit Holder.

Fee

| TYPE OF FEE | RATE |

|---|---|

| Registration | RM180 |

| Additional Registration | RM90 |

| Revocation | RM70 |

| Change of Hibah Donee/ Hibah Guardian/ Addition or removal of Fund | RM20 |

| Administration | RM10 Annually |

| Administration to Claim | |

|---|---|

| BALANCE OF INVESTMENT (RM) | RATE |

| First 25,000 | 1.50% |

| The Next 225,000 | 1.00% |

| The Next 250,000 | 0.50% |

| The Next 500,000 | 0.25% |

| The Remaining Balance | 0.10% |

Calculation of Claim Fee

Example:

Investment holding balance RM200,000

| First RM25,000 | 1.50% = RM375 |

| Remaining RM175,000 | 1.00% = RM1,750 |

| Total Fees | = RM2,125 |

| (Fees will be deducted from investment holding balances based on the current rate when distribution is paid to Hibah Donees) | |

FAQ

Hibah Amanah is the combination of "hibah" and trust concepts. It is a gift in the form of ASNB unit trust fund (Hibah Asset) from a Unit Holder (Donor) to his loved ones Donee(s) during his lifetime based on the terms and conditions stated in the Hibah Deed. Transfer of the asset to the Donee(s) takes effect only after the demise of the Donor.

Hibah Asset is the ASNB unit trust fund(s) registered under Hibah Amanah by the Donor during his lifetime through the Hibah Amanah Deed:

The fund(s) registered must be given to the donee(s) in its entirely (100%)

To be eligible, the balance units of each unit trust fund must be 1,000 units and above throughout the period of Hibah Amanah

The units must be wholly-owned by the donor

Under the Malaysian law, the trust is classified as personal property such as company shares. Thus, the inheritance of unit trusts is subject to the laws of probate and administration where only the administrator or executor appointed by the court can claim the deceased donor's assets. On the other hand, EPF and Tabung Haji were established under their own acts that allow direct nominees.

Without an alternative solution like Hibah Amanah, the estate distribution process is complicated and time-consuming. The situation will be more complicated if there are overlapping claims and disagreement among the beneficiaries.

Through Hibah Amanah, unit holders can plan their estate distribution to their beneficiaries and this will shorten the claim process after their demise.

Hibah Amanah is based on the Sharia law. However, Faraidh law still prevails in the estate distribution for Muslims. Therefore, unit holders are advised to be fair in distributing their Hibah assets.

Eligibility of Applicant/Donor/Eligibility of Donee/Revocation

A. Eligibility of Applicant/Donor

- ASNB's unit holders

- Malaysian

- Age 18 and above

- Muslim

- Not a bankrupt

- Sound mind

- The Trust Declaration is automatically revoked

- The unit trust funds will then be frozen

- The rights of the Donor will be determined by the Bankruptcy Law following the Insolvency Department's instructions, and so on

A guardian must be appointed by the court who will be acting on behalf of the Donor based on the court's order.

B. Eligibility of Donee

- Donor can name any individual as a Donee limited to 10 persons per contract

- Not a bankrupt

- Donee is not a bankrupt at the time of payment of claim

- The donee is encouraged to register as a unit holder with ASNB, if eligible =

- Open to Malaysian or non-Malaysian

- Sound Mind

- Open to all religions

Yes, but a guardian must be appointed to act on behalf of the minor Donee, age 18 and above or special need. The appointed guardian must be among:

- parents

- grandparents

- siblings

- registered guardian approved by ASNB

C. Registration

Registration can be performed at any ASNB branch and selected/permitted agents (for first registration only).

Complete the following documents and submit with the registration fee:

- Application form (PH1A)

- One original copy of Power of Attorney

Yes, the Ijab and Qabul are compulsory; therefore, both the Donor and Donee must agree to give and accept by signing the relevant documents.

Yes, subject to the minimum balance of 1,000 units throughout the period of Hibah Amanah.

Yes, subject to the minimum balance of 1,000 units throughout the period of Hibah Amanah.

D. Distribution of Hibah Asset

All the units in each trust fund will be distributed to the Donee(s) in its entirely (100%).

Example: The Donor has an investment in the ASN Imbang 2 fund. He must distribute 100% of the units to the listed Donee(s) as follows:

ASN Imbang 2 (100%)

- Donee A - 20%

- Donee B - 30%

- Donee C - 50%

Yes. However, changes can only be made if it involves biological child and grandchildren. Otherwise, the revocation of the Hibah Amanah must be made and the Letter of Donee consent on return of asset to Donor must be submitted during application.

E. Administration Fee

Administration Fee is charged annually for administration, data and document archiving for Hibah Amanah. This fee is waived for the first year of registration at the discretion of ASNB.

The annual administration fee is RM10.

From 01/12/2021 Administration Fee will be charged on the second year of registration as follows:

| No | Scenario | Method for Administration Fee |

|---|---|---|

| 1 | Income distribution received from the fund selected for Administration Fee during registration is higher than the Administration Fee | Deduction from income distribution of ASNB fund selected for Administration Fee during registration; or |

| 2 | Income distribution received from the fund selected for Administration Fee during registration is lower than the Administration Fee | Deduction from principle units (excludes blocked units) of the selected fund for Administration Fee; or |

| 3 | Fund selected for Administration Fee during registration is not eligible for income distribution. | Deduction from principle units (excludes blocked units) of the selected fund for Administration Fee; or |

| 4 |

| Deduction from the 1,000 units blocked during Hibah Amanah registration. If the deduction was from the 1,000 blocked unit, the amount will be topped up from future income distribution (if any) |

deduction from income distribution (if any) of ASNB fund selected for Administration Fee during registration; or

deduction from principle unit of the selected fund for Administration Fee; or

- deduction from the 1,000 units blocked during Hibah Amanah registration. If the deduction was from the 1,000 blocked unit, the amount will be topped up from future income distribution (if any).

No, this method will only be applicable for new registrations with effect from 01/12/2021.

No. The Donor may not change the unit trust fund previously selected for annual Administration Fee deduction.

F. Claim and Payment

In the event the Donor dies first, the Hibah asset will be the absolute right of the Donee(s). On the other hand, if the Donee(s) dies first, the ownership of the Hibah asset will be returned to the Donor. If the Hibah Donor & the Hibah Donee die simultaneously the Hibah Asset will be paid according to the current procedure of the estate.

Units invested via financing is subjected to the agreement between the Donor and the Financing provider. Units still under financing will be paid to the Financing provider. Only the Donor's wholly-owned units free from encumberance will be distributed to the Donee upon claim.

G. Revocation of Hibah Amanah

Based on Sharia law, Hibah Amanah cannot be revoked, except if it involves hibah to biological child or grandchild.